State of the Biz Av Economy, Part 4 of 3 (or something like that!)

In this concluding (I promise!) examination of the aviation business climate, I thought I'd summarize with some articles from significant observers/participants in the industry, following our review of Molly McMillin's Wichita Eagle article from last week.

(Partly prompted by Friday's sad news of another 240 job cuts at HawkerBeech; "Friday's WARN notices put the number of layoffs at HBC in the past 10 months at 3,553, or about 36 percent of last October's total work force."

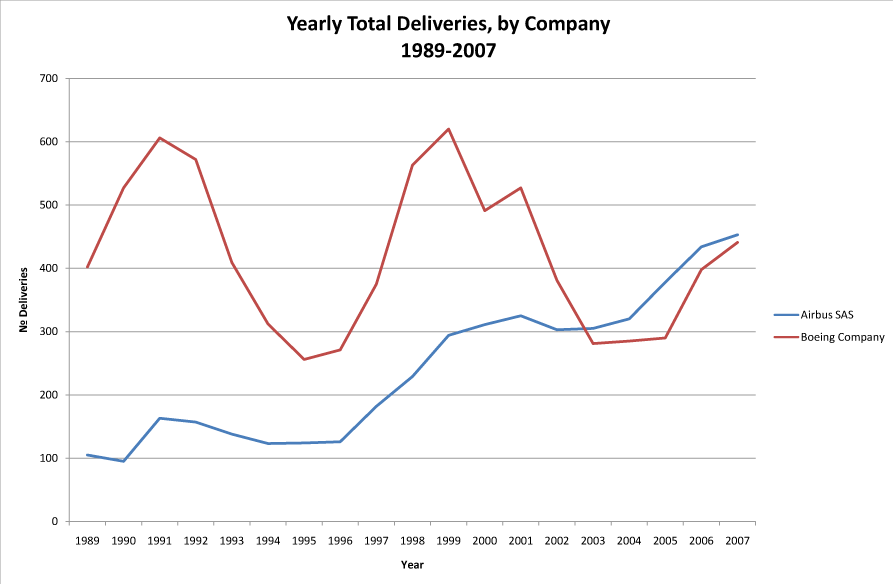

Aviation Week reviewed the GA market in their Aug 10 article "GA Shipments Continue Downward Spiral". ("The second quarter of 2009 further compounded the economic woes of the general aviation manufacturing sector as the number of deliveries plunged some 49 percent, according to statistics released last week by the General Aviation Manufacturers Association. This has led to a 45.9 percent decline in total deliveries through the first half of the year.")The Aviation Week Intelligence Network had coverage (Sept 23) of Wichita Suffers From Bizjet Downturn. "A severe downturn in the aviation industry has led to the loss of 30,000 jobs in Wichita as the impact from mass layoffs at companies such as Cessna, Hawker Beechcraft and Bombardier Learjet has rippled through small suppliers and the economy, according to Mayor Carl Brewer."

Our friend Richard Aboulafia, of the Teal Group, recently had an EXCELLENT two-part expose' of the state of affairs-

TEAL GROUP BIZAV OVERVIEW (PART 1)

("Our forecast assumes a three-year downturn. The key demand drivers – economic growth and corporate profits – will only recover in late 2010. It will take some time to reduce record inventories of available jets for sale. This means new business jet deliveries won’t start to recover until 2012. The trough year of our forecast – 2011 – will see business jet deliveries reduced by 40% relative to 2008. Our forecast then calls for a five-year recovery period with 10% growth per year starting in 2012.")

TEAL GROUP BUSINESS AVIATION OVERVIEW (PART 2) ("A closer look at the driving factors.")

Chad Trautvetter had a nice Sept piece in Aviation International News (AIN), which captures a quote many will be relieved to hear

UBS: Bizjet Market ‘Less Worse, Not Better’

But, as a note of caution, I will refresh our memories with Honeywell's Oct 2008 outlook (sorry, somebody there is cringing, or worse):

"The 2008 survey indicates record aircraft deliveries will continue into 2009 with a likely peak next year or in 2010...The stability in overall purchase expectations is supported by the increasingly global nature of the industry."

(Ah yes, I remember that widely repeated refrain- something like "the global demand for biz jets will damp out the US cyclical demand". Boy, that's so obviously erroneous in hindsight- but at the time, .I have to admit, it sounded reasonable to me too...).

To add insult to injury, or rather, injury to insult, Honeywell did not only not see their customer's market declining, they didn't even see their own market declining. From July 27, 2009: "Honeywell 2nd-Qtr earnings drop 38 percent as recession continues to take toll" (Oops. It will be interesting to see what the "18th Business Aviation Outlook" forecast says- should be out in a few weeks).

Bombardier has an aviation business forecast too, good reading,

Bombardier Business Aircraft Forecast 2009-2018

"Bombardier remains confident that there is strong

potential for the business jet industry over the next 10 years.".

(A bit understated, not nearly as disruptive as some forecasts we've heard in the past... :)

Let's hope for our friends in the industry, that better times are coming soon...

{kind=link}

{kind=link}

{kind=link}